This is republished content originally hosted on the Mercatus’ Center former blog, Neighborhood Effects.

This fall eligible Alaskans will be receiving a check of $1,100 from their state government. Although the amount of the check can vary, Alaskans receive one every fall – no strings attached. Other state residents are probably more familiar with IRS tax refunds that come every spring, but this “tax refund” that Alaskans receive is unique. It’s a feature that residents have benefited from for decades, even in times when the government has experienced fiscal stress. Considering the state’s unique and distressed budget situation that I’ve described in an earlier post, I think it warrants a discussion of the fiscal viability of their refunds.

A narrow tax base reliant on volatile revenue sources, restricted funds, and growing spending are all factors that made closing Alaska’s budget gap this year very difficult. It even contributed to pulling down Alaska from 1st in our 2016 ranking of states by fiscal condition to 17th in our 2017 edition. Given this deterioration, it will be helpful to look into how and why Alaska residents receive dividend payments each year. There is no public finance rule that says giving refunds to residents is fiscally irresponsible, but there definitely are better ways to do it, and Alaska certainly hasn’t proven to display best practices.

Another state that we can look at for comparison is Colorado, which has a similar “tax refund” for residents but is structured very differently. Colorado’s Taxpayer Bill of Rights (TABOR) requires that higher than expected tax revenues each year be refunded to taxpayers and acts as a restraint on government spending growth. In contrast, Alaska’s check comes from the state’s Permanent Fund’s earnings that are generated from oil severance taxes each year, and acts more like a dividend from oil investment earnings.

Are distributing these refunds to taxpayers fiscally responsible? I am going to take a deeper look at these mechanisms to find out.

First, Alaska’s refund.

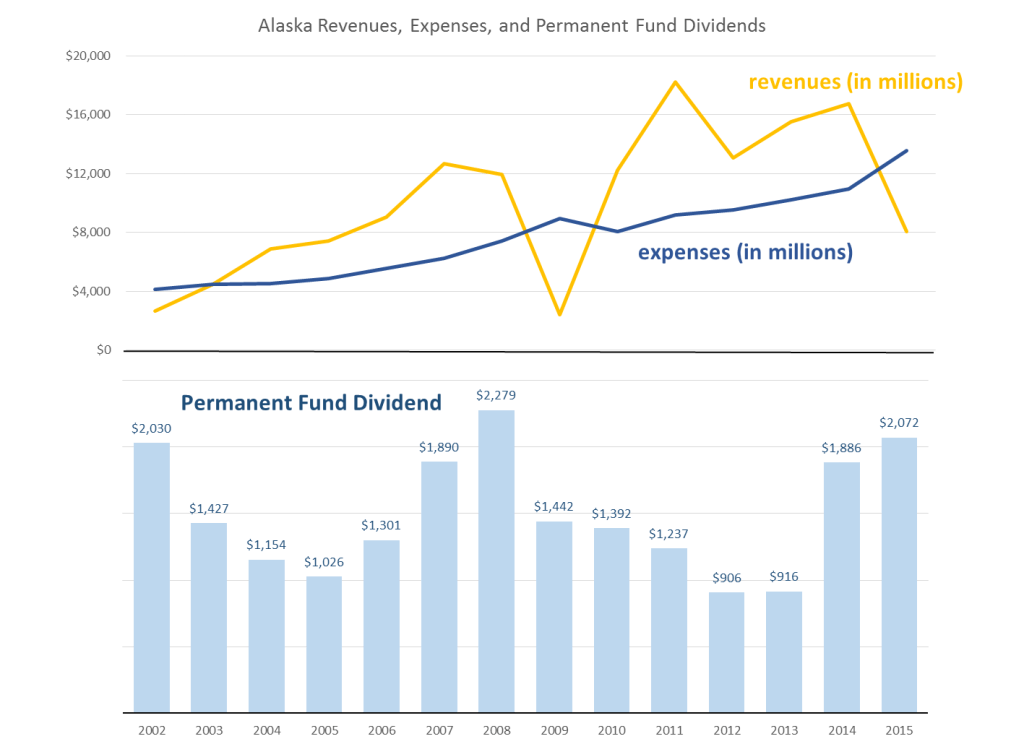

The figure below displays Alaska’s Permanent Fund checks since 2002 overlaid with the state’s revenue and expenditure trends, all adjusted for inflation. The highest check (in 2015 dollars) was $2,279 in 2008 and the lowest was $906 in 2012, with the average over this time period being about $1,497 per person. Although the check amounts do vary, Alaska has kept on top of delivering them, even in times of steep budget gaps like in 2002, 2009, and 2015. The Permanent Fund dividend formula is based on net income from the current plus the previous four fiscal years, so it makes sense that the check sizes are also cyclical in nature, albeit in a slightly delayed fashion behind oil revenue fluctuations.

Alaska’s dividend payments often end up on the chopping block during yearly budget debates, and there is growing pressure to at least have them reduced. Despite this, Alaska’s dividends are very popular with residents (who can blame them?) and probably won’t be going away for a long time; bringing a new meaning to the Permanent Fund’s name.

The Alaska Permanent Fund was established in 1976 by constitutional amendment and was seen as an investment in future generations, who might no longer have access to oil as a resource. Although this may have been decent forward-thinking, which is rare in state budgets, it does illustrate an interesting public finance story.

Alaska is a great example of a somewhat backwards situation. They generate high amounts of cash each year, but because of the way many of their funds are restricted they are forced to hoard much of it, and give the rest to citizens in the form of dividends. If a different state were to consider a similar dividend before dealing with serious structural budget flaws would be akin to putting the cart before the horse.

Luckily for Alaskan dividend recipients, there are many other areas that the state could reform first in order to improve their budget situation while avoiding cutting payments. As my colleague Adam Millsap has recommended, a fruitful area is tax reform. Alaska doesn’t have an income or sales tax; two of the most common sources of revenue for state governments. These are two potentially more stable sources of income than what the state currently has.

How does Colorado’s “tax refund” compare?

Colorado’s Taxpayer Bill of Rights (TABOR) has a feature that requires any tax revenue growth beyond inflation and population growth be refunded to taxpayers. It was adopted by Colorado voters in 1992 and it essentially restricts revenues by prohibiting any tax or spending increases without voter approval.

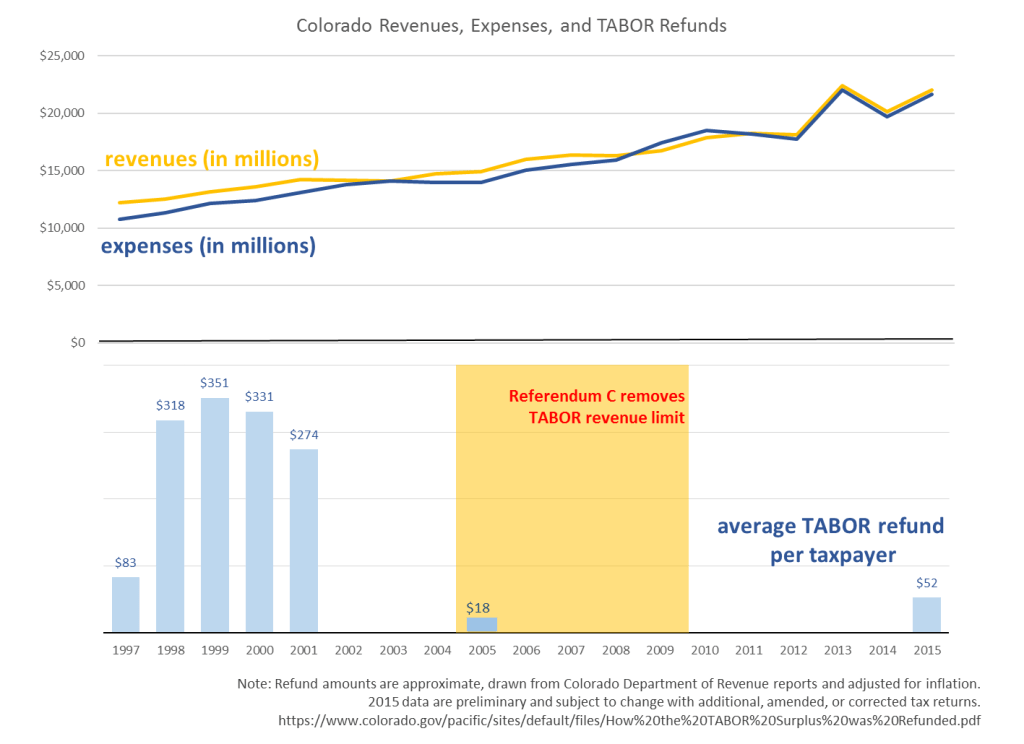

A recent example of this playing out was in 2014 when the state realized higher than expected tax revenues as a result of marijuana legalization. At the point of legalization, the plan was to direct tax revenues generated from the sale of marijuana towards schools or substance abuse program funding. But because of the higher than expected revenues, TABOR was triggered and it would require voter approval to decide if the excess revenues would be sent back to taxpayers or directed to other state programs.

In November of 2015, Colorado voters approved a statewide ballot measure that gave state lawmakers permission to spend $66.1 million in taxes collected from the sale of marijuana. The first $40 million was sent to school construction, the next $12 million to youth and substance abuse programs, and the remainder $14.2 billion to discretionary spending programs. A great example that although TABOR does generally restrain spending, citizens still have power to decline refunds in the name of program spending they are passionate about.

The second figure here displays TABOR refunds compared with state revenues and expenditures over time. Adjusted for inflation, checks have varied from $18 in 2005 to $351 in 1999, much smaller than the Alaska dividend checks. TABOR checks have only tended to be distributed when revenues have exceeded expenses. The main reason why checks weren’t distributed between 2006 and 2009, despite a revenue surplus, was because of Referendum C which removed TABOR’s revenue limit for five years, allowing the state to keep collections exceeding the rule. The revenue limit has since been reinstated, but some question the effectiveness of TABOR given an earlier amendment in 2000 which exempts much of education spending from TABOR restrictions.

The main distinguishing factor between Colorado’s refund and Alaska’s Permanent Fund dividend is that the former also acts as a constraint on spending growth. By requiring the legislature to get voter approval before any tax increase or spending of new money, it implements automatic checks on these activities. Many states attempt to do this through what are called “Tax and Expenditure Limits” or TELs.

The worry is that left unchecked, state spending can grow to unsustainable levels.

Tax and Expenditure Limits

A review of the literature up to 2012 found that although the earliest studies were largely skeptical of the effectiveness of TELs, as time has passed more research points to the contrary. TELs can restrain spending, but only in certain circumstances.

My colleague Matt Mitchell found in 2010 that TELs are more effective when they (1) bind spending rather than revenue, (2) require a super-majority rather than a simple majority vote to be overridden, (3) immediately refund revenue collected in excess of the limit, and (4) prohibit unfunded mandates on local government.

Applying these criteria to Colorado’s TABOR we see that it does well in some areas and could improve in others. TABOR’s biggest strength is that it immediately refunds revenue collected in excess of the limit in its formula, pending voter approval to do otherwise. Automatically refunding surpluses makes it difficult for governments to use excess funds irresponsibly and also gives taxpayers an incentive to support TABOR.

Colorado’s TABOR does well to limit revenue growth according to a formula, rather than to a fixed number or no limitation at all. The formula partially meets Mitchell’s standards. It stands up well with the most stringent TELs by limiting government growth that exceeds inflation and population growth, but could actually be improved if it limited actual spending growth rather than focusing on tax revenue. When a TEL or similar law limits revenues, policymakers can respond by resorting to implementing more fees or borrowing. There’s some evidence of this occurring in Colorado, with fees becoming more popular as a way to raise revenue since TABOR’s passing. A spending-based TEL is more difficult to evade.

Despite its faults, Colorado’s TABOR structure appears to be doing better than attempts to constrain spending growth in other states. The National Conference of State Legislatures still considers it one of the strictest TELs in the nation. Other states, like Arkansas, could learn a lot from Colorado. A recent Mercatus study analyzes Arkansas’ Revenue Stabilization Law and suggests that it is missing a component similar to Colorado’s TABOR formula to refund excess revenues.

How much a state spends is ultimately up to its residents and legislature. Some states may have a preference for more spending than others, but given the tendency for government spending to grow towards an unsustainable direction, having a conversation about how to slow this is key. Implementing TEL-like checks allows for spending to be monitored and that tax dollars be spent more strategically.

Alaska’s Permanent Fund dividend is not structured as well as Colorado’s, but perhaps the state’s saving grace is that it has a relatively well structured TEL. Similarly to Colorado’s TABOR, Alaska’s TEL limits budget growth to the sum of inflation and population growth and is codified in the constitution. Alaska’s TEL doesn’t immediately refund revenue that is collected in excess of the limit to taxpayers as Colorado’s TABOR does, but it does target spending rather than revenues.

Colorado’s and Alaska’s TELs can compete when it comes to restraining spending, but Colorado’s is certainly more strict. Colorado’s expenditures have grown by about 55 percent over the last decade, while Alaska’s has grown approximately 120 percent.

The Lesson

Comparing Colorado and Alaska’s situations reveals two different ways of giving tax refunds to residents. Doing so doesn’t necessarily have to be fiscally irresponsible. Colorado has provided refunds to residents when state revenues have exceeded expenses and as a result this has acted as a restraint on over-spending higher than expected revenues. Although Colorado’s TABOR has been amended over time, its general structure illustrates the effectiveness of institutional restrains on spending. The unintended effects of TABOR, such as the increase in fees, could be well addressed by specifically targeting spending rather revenue, like in the case of Alaska’s TEL. Alaska may have had their future residents’ best intent in mind when they designed their Permanent Fund Dividend, but perhaps this goal of passing forward oil investment earnings should have been paired with preparing for the potential of cyclical budget woes.